Euro area quarterly balance of payments and international investment position: fourth quarter of 2024

4 April 2025

- Current account surplus at €426 billion (2.8% of euro area GDP) in 2024, after a €243 billion surplus (1.7% of GDP) a year earlier.

- Geographical counterparts: largest bilateral current account surpluses vis-à-vis United Kingdom (€197 billion) and Switzerland (€76 billion) and largest deficit vis-à-vis China (€105 billion).

- International investment position showed net assets of €1.66 trillion (10.9% of euro area GDP) at end of 2024.

- Bilateral current account vis-à-vis the United States: surplus of €3 billion (0.0% of euro area GDP) in 2024, following a deficit of €30 billion (0.2% of GDP) in 2023. For more details see dedicated section on economic and financial linkages between the euro area and the United States.

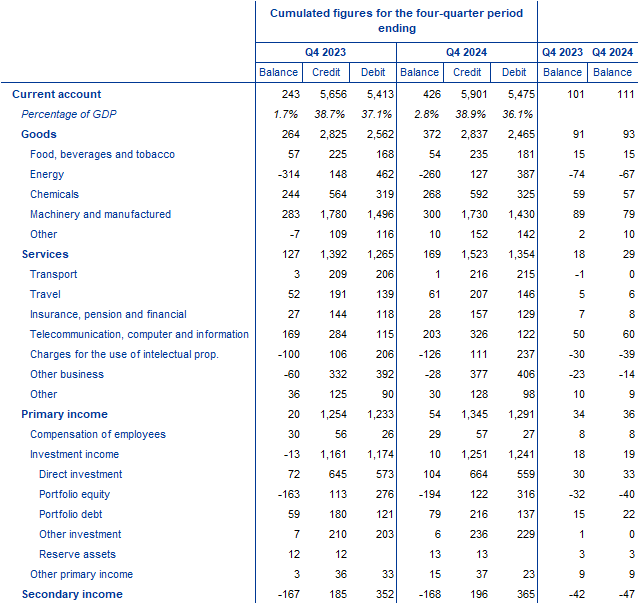

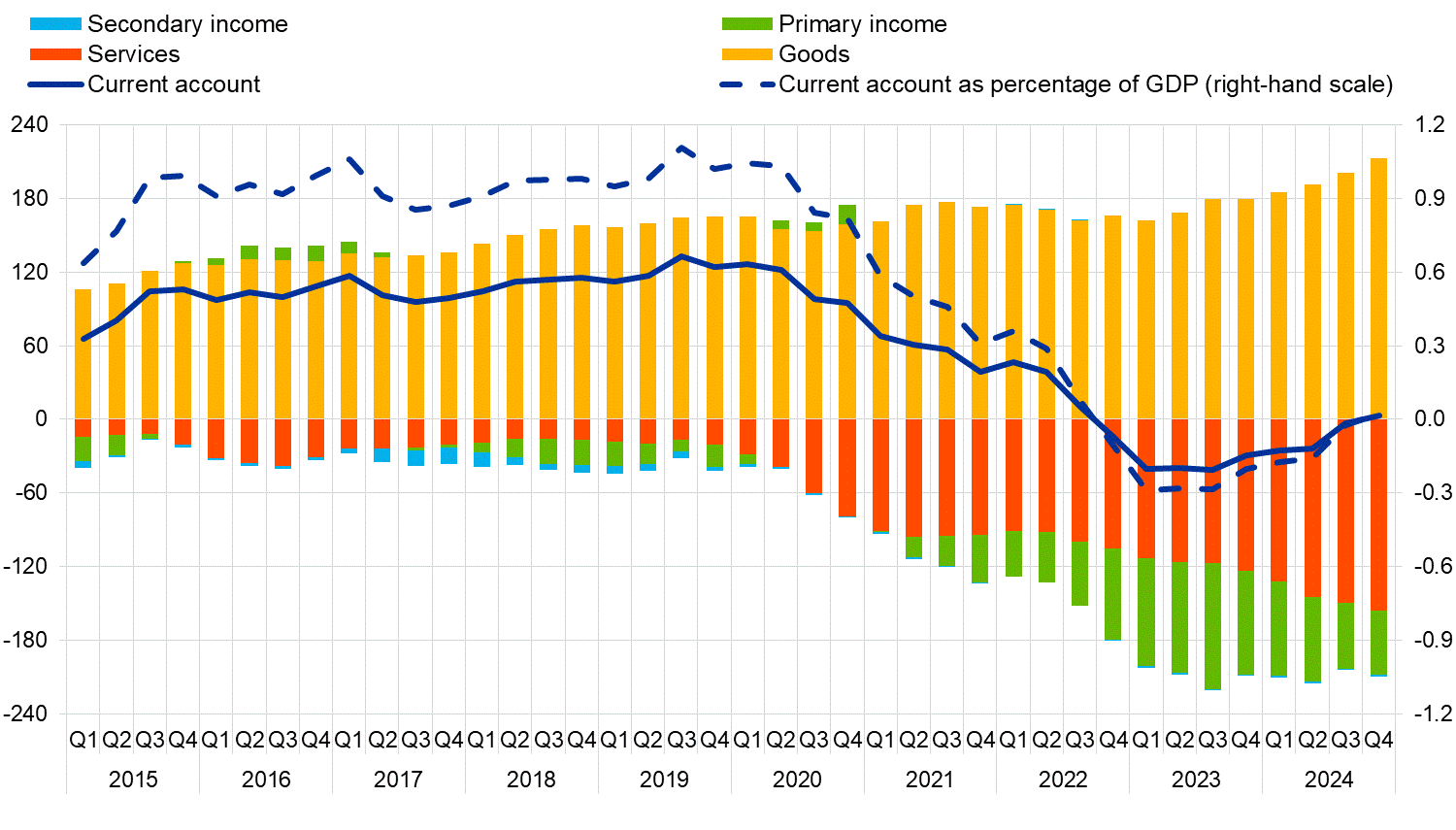

Current account

The current account of the euro area recorded a surplus of €426 billion (2.8% of euro area GDP) in 2024, following a €243 billion surplus (1.7% of GDP) a year earlier (Table 1). This development was driven by larger surpluses for goods (from €264 billion to €372 billion), services (from €127 billion to €169 billion) and primary income (from €20 billion to €54 billion). The deficit for secondary income increased moderately from €167 billion to €168 billion.

The estimates on goods trade broken down by product group show that in 2024 the increase in the goods surplus was mainly due to a reduction in the deficit for energy products (from €314 billion to €260 billion). In addition, the surpluses for chemical products and machinery and manufactured products increased (from €244 billion to €268 billion and from 283 billion to €300 billion, respectively).

The larger surplus for services in 2024 was mainly due to widening surpluses for telecommunication, computer and information (from €169 billion to €203 billion) and travel (from €52 billion to €61 billion), and a lower deficit for other business services (from €60 billion to €28 billion). These developments were partly offset by a widening deficit for charges for the use of intellectual property (from €100 billion to €126 billion).

In 2024, the increase in the primary income surplus was mainly due to larger surpluses in direct investment (from €72 billion to €104 billion), portfolio debt (from €59 billion to €79 billion), and other primary income (from €3 billion to €15 billion), which were partly offset by a larger deficit in portfolio equity (from €163 billion to €194 billion).

Table 1

Current account of the euro area

(EUR billions, unless otherwise indicated; transactions during the period; non-working day and non-seasonally adjusted)

Source: ECB.

Notes: “Equity” comprises equity and investment fund shares. Goods by product group is an estimated breakdown using a method based on statistics on international trade in goods. Discrepancies between totals and their components may arise from rounding.

Data on the geographical counterparts of the euro area current account (Chart 1) show that in 2024, the euro area recorded its largest bilateral surpluses vis-à-vis the United Kingdom (€197 billion, down from €220 billion a year earlier) and Switzerland (€76 billion, up from €65 billion). The euro area also recorded surpluses vis-à-vis other emerging countries (€155 billion, up from €135 billion a year earlier) and other advanced countries (€114 billion, up from €80 billion). The largest bilateral deficit was recorded vis-à-vis China (€105 billion, down from €109 billion a year earlier) and a deficit was also recorded vis-à-vis the residual group of other countries (€96 billion, down from €142 billion).

The most significant changes in the geographical components of the current account in 2024 relative to 2023 were as follows: the goods surpluses increased vis-à-vis the United States (from €179 billion to €213 billion) and vis-à-vis other advanced countries (from €27 billion to €50 billion), while the goods deficit vis-à-vis China increased from €131 billion to €141 billion. In services, the deficit vis-à-vis the United States increased (from €124 billion to €156 billion), while the balance vis-à-vis offshore centres shifted from a deficit (€8 billion) to a surplus (€16 billion). In primary income, the balance vis-à-vis the United Kingdom shifted from a surplus (€31 billion) to a deficit (€4 billion) while a smaller deficit was recorded vis-à-vis the United States (from €84 billion to €52 billion). The deficit in secondary income vis-à-vis the EU Member States and EU institutions outside the euro area decreased slightly (from €76 billion to €73 billion).

Chart 1

Geographical breakdown of the euro area current account balance

(four-quarter moving sums in EUR billions; non-seasonally adjusted)

Source: ECB.

Note: “EU non-EA” comprises the non-euro area EU Member States and those EU institutions and bodies that are considered for statistical purposes as being outside the euro area, such as the European Commission and the European Investment Bank. “Other advanced” includes Australia, Canada, Japan, Norway and South Korea. “Other emerging” includes Argentina, Brazil, India, Indonesia, Mexico, Saudi Arabia, South Africa and Türkiye. “Other countries” includes all countries and country groups not shown in the chart, as well as unallocated transactions.

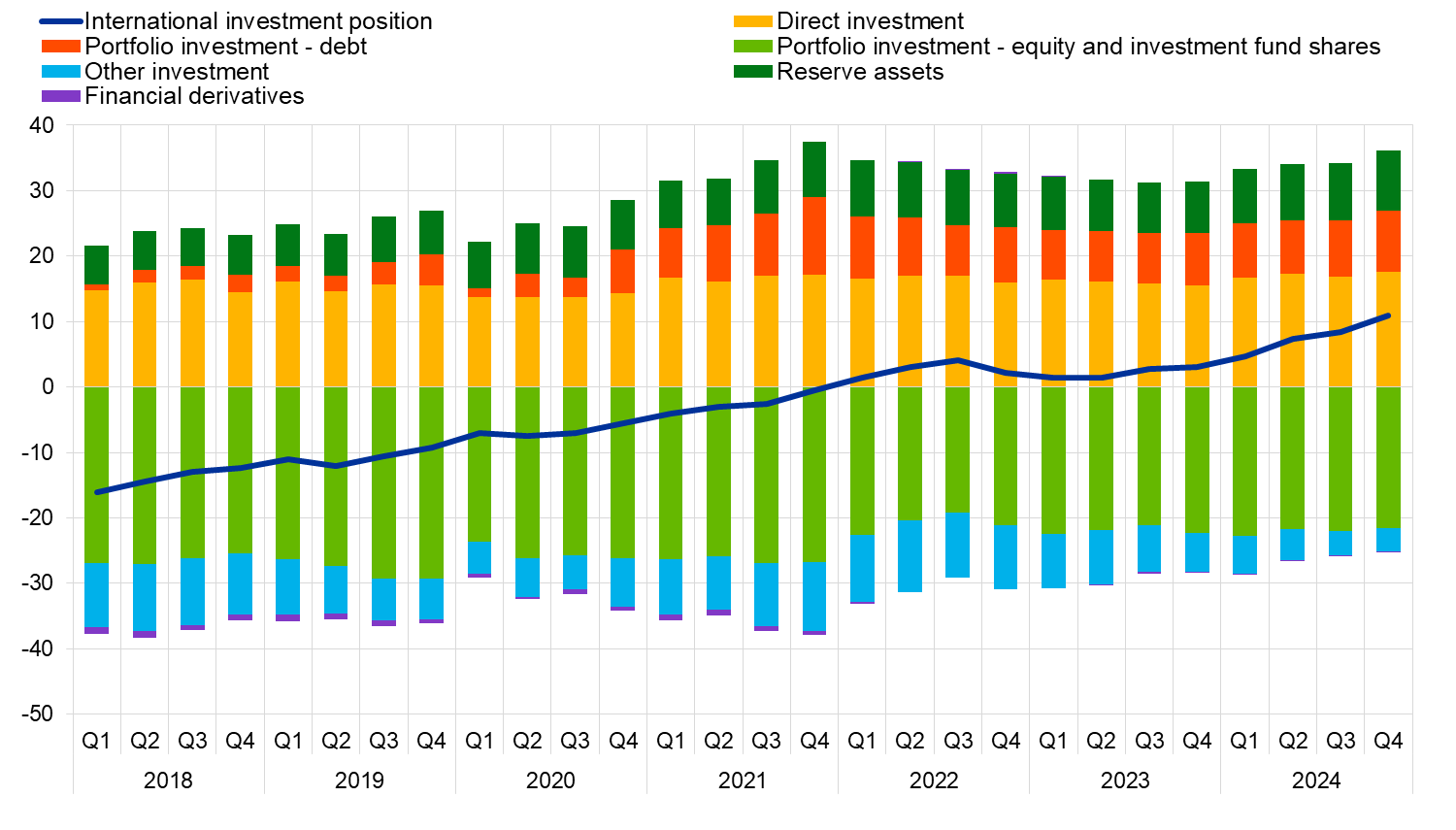

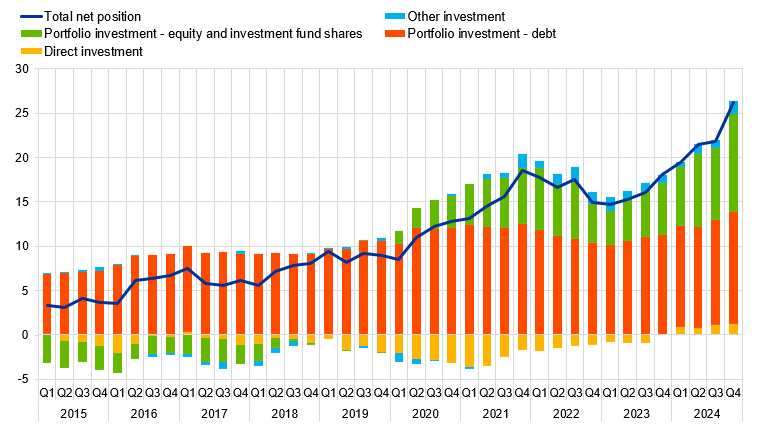

International investment position

At the end of 2024, the international investment position of the euro area recorded net assets of €1.66 trillion vis-à-vis the rest of the world (10.9 % of euro area GDP), up from €1.25 trillion in the previous quarter (Chart 2 and Table 2).

Chart 2

Net international investment position of the euro area

(net amounts outstanding at the end of the period as a percentage of four-quarter moving sums of GDP)

Source: ECB.

The €407 billion increase in net assets was mainly driven by larger net assets in portfolio debt (up from €1.27 trillion to €1.42 trillion), direct investment (up from €2.54 trillion to €2.66 trillion) and reserve assets (up from €1.32 trillion to €1.39 trillion).

Table 2

International investment position of the euro area

(EUR billions, unless otherwise indicated; amounts outstanding at the end of the period, flows during the period; non-working day and non-seasonally adjusted)

Source: ECB.

Notes: “Equity” comprises equity and investment fund shares. Net financial derivatives are reported under assets. “Other volume changes” mainly reflect reclassifications and data enhancements. Discrepancies between totals and their components may arise from rounding.

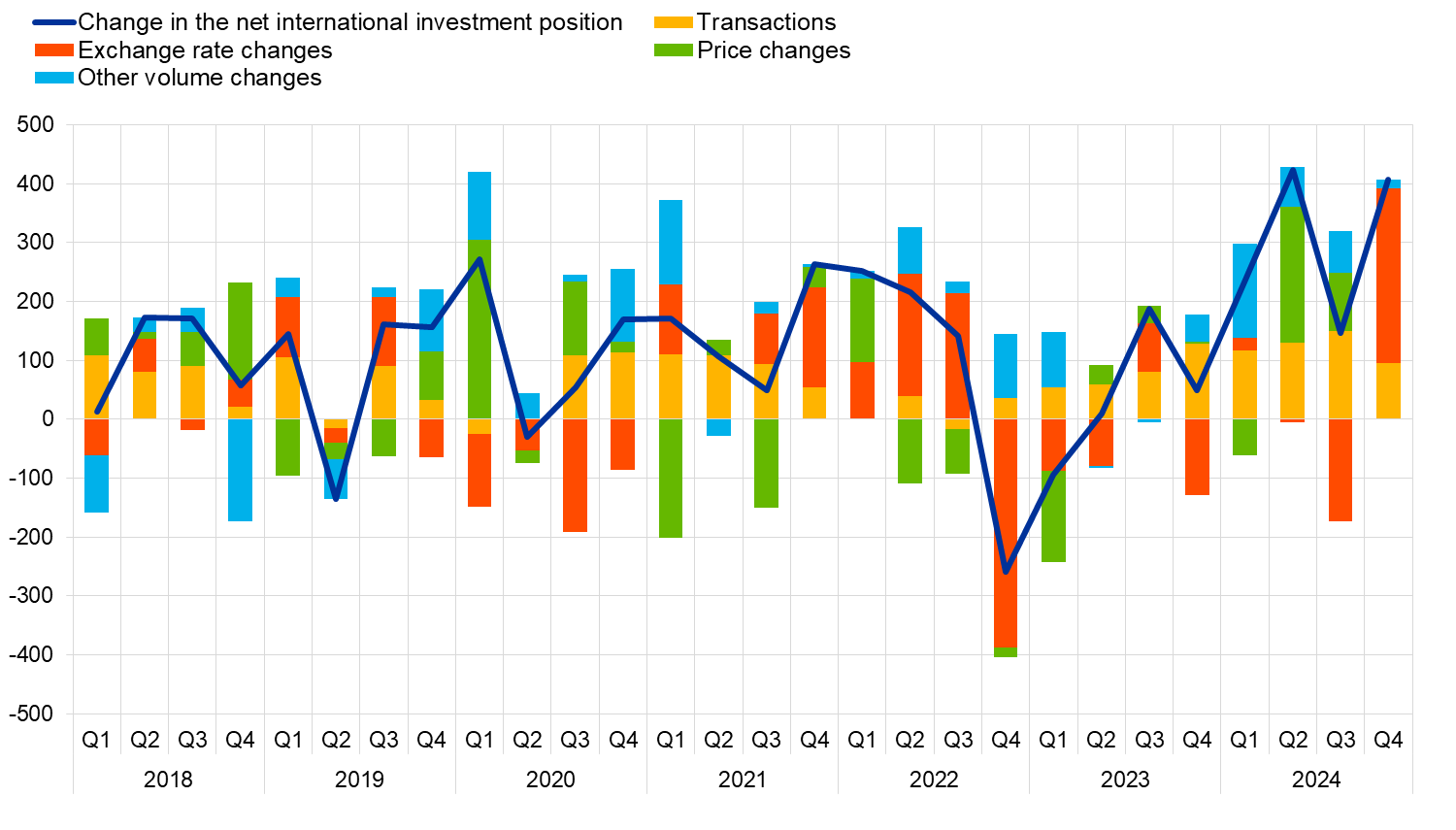

The developments in the euro area’s net international investment position in the fourth quarter of 2024 were driven mainly by positive exchange rate changes, and to a lesser extent by positive transactions and other volume changes (Table 2 and Chart 3).

At the end of the fourth quarter of 2024, direct investment assets of special purpose entities (SPEs) amounted to €3.58 trillion (28% of total euro area direct investment assets), up from €3.53 trillion at the end of the previous quarter (Table 2). Over the same period, direct investment liabilities of SPEs increased from €3.10 trillion to €3.13 trillion (31% of total direct investment liabilities).

At the end of the fourth quarter of 2024 the gross external debt of the euro area amounted to €16.70 trillion (110% of euro area GDP), up by €1 billion compared with the previous quarter.

Chart 3

Changes in the net international investment position of the euro area

(EUR billions; flows during the period; non-working day and non-seasonally adjusted)

Source: ECB.

Note: “Other volume changes” mainly reflect reclassifications and data enhancements.

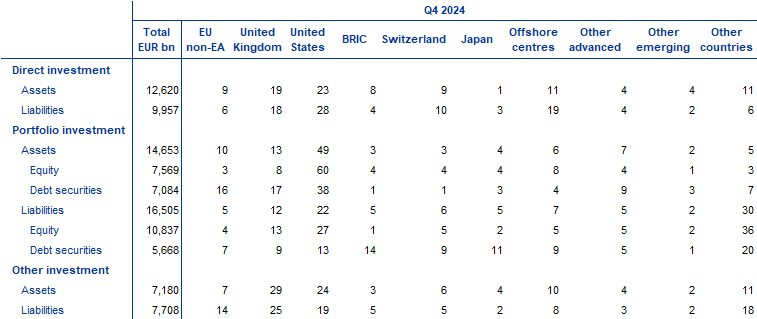

At the end of 2024 euro area direct investment assets were €12.62 trillion, 23% of which was invested in the United States and 19% in the United Kingdom (see Table 3). Euro area direct investment liabilities were €9.96 trillion, with 28% being investments from the United States, 19% from offshore centres and 18% from the United Kingdom.

In portfolio investment, euro area holdings of foreign securities amounted to €7.57 trillion in equity and €7.09 trillion in debt securities at the end of 2024. The largest holdings of equity were in securities issued by residents of the United States (accounting for 60%). In debt securities, the largest euro area holdings were in securities issued by residents of the United States (accounting for 38%), the United Kingdom (17%) and the EU Member States and EU institutions outside the euro area (16%).

On the portfolio investment liabilities side, non-residents’ holdings of securities issued by euro area residents stood at €10.84 trillion in equity and at €5.67 trillion in debt at the end of 2024. The largest holder countries of euro area equity were the United States (27%) and the United Kingdom (13%), while for euro area debt securities the largest holders were the BRIC group of countries (14%), the United States (13%) and Japan (11%).

In other investment, euro area residents’ claims on non-residents amounted to €7.18 trillion, 29% of which was vis-à-vis the United Kingdom and 24% vis-à-vis the United States. Euro area other investment liabilities amounted to €7.71 trillion, with the United Kingdom accounting for 25% and the United States for 19%.

Table 3

International investment position of the euro area – geographical breakdown

(as a percentage of the total, unless otherwise indicated; at the end of the period; non-working day and non-seasonally adjusted)

Source: ECB.

Notes: “Equity” comprises equity and investment fund shares. “EU non-EA” comprises the non-euro area EU Member States and those EU institutions and bodies that are considered for statistical purposes as being outside the euro area, such as the European Commission and the European Investment Bank. The “BRIC” countries are Brazil, Russia, India and China. “Other advanced” includes Australia, Canada, Norway and South Korea. “Other emerging” includes Argentina, Indonesia, Mexico, Saudi Arabia, South Africa and Türkiye. “Other countries” includes all countries and country groups not listed in the table as well as unallocated positions.

Economic and financial linkages between the euro area and the United States

This statistical release provides a longer-term perspective on the euro area’s bilateral current account balance and international investment position vis-à-vis the United States by presenting developments over the past decade.

In 2024 the euro area recorded a current account surplus of €3 billion (0.0% of euro area GDP) vis-à-vis the United States, following a deficit of €30 billion (0.2% of GDP) in 2023 (see Chart 4). The euro area had recorded a rather stable current account surplus vis-à-vis the United States of around 1.0% of GDP between 2015 and 2019, which gradually declined subsequently and turned into a deficit in 2022. Since 2015 the euro area has run a persistent and sizeable goods surplus vis-à-vis the United States, rising from €127 billion in 2015 to €213 billion in 2024. The marked decline in the euro area current account surplus vis-à-vis the United States over the past decade was mainly due to a pronounced widening in the deficit for services (from €21 billion in 2015 to €156 billion in 2024), driven by an increasing deficit in charges for the use of intellectual property (from €5 billion to €168 billion). In addition, the euro area’s primary income balance vis-à-vis the United States changed from a surplus of €2 billion in 2015 to a deficit of €52 billion in 2024, largely due to a widening deficit in direct investment income. The developments in the euro area’s bilateral current account balance vis-à-vis the United States, in particular the significant changes observed since 2019, are partly connected to the activities of US multinational enterprises in the euro area.

Chart 4

Euro area current account balance vis-à-vis the United States

(left-hand scale: four-quarter moving sums in EUR billions; right-hand scale: four-quarter moving sums as a percentage of GDP; non-seasonally adjusted)

Source: ECB.

At the end of 2024, the euro area’s bilateral investment position vis-à-vis the United States showed net assets equivalent to 26% of euro area GDP, up from 18% of GDP at the end of 2023 and 4% of GDP at the end of 2015 (Chart 5). Net asset positions in portfolio investment debt (13% of GDP) and portfolio investment equity (11% of GDP) contributed most to the euro area’s bilateral net asset position at the end of 2024. The increase in the euro area bilateral net asset position since 2015 was driven mainly by a shift in portfolio investment equity from a net debtor to a net creditor position, as euro area portfolio investment equity assets vis-à-vis the United States rose more strongly than the corresponding liabilities. Developments in portfolio investment debt and direct investment also contributed, albeit to a lesser extent, to the increase in total net assets vis-à-vis the United States.

Chart 5

Euro area net investment position vis-à-vis the United States

(net amounts outstanding at the end of the period as a percentage of four-quarter moving sums of GDP)

Source: ECB.

Notes: “Total net position” refers to the sum of net direct investment, net portfolio investment, net other investment and net financial derivatives. Reserve assets are not included in the total. Net positions are computed as the asset positions minus the liability positions of the respective item. Discrepancies between totals and their components may arise from rounding.

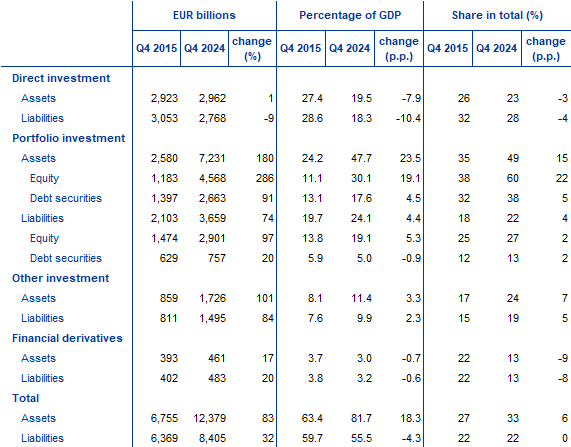

The United States is the largest destination country for euro area cross-border financial investment. Euro area financial assets vis-à-vis the United States amounted to €12.38 trillion at the end of 2024 (82% of euro area GDP), with an 83% increase since the end of 2015 (see Table 4). This development increased the share of the United States in euro area external assets from 27% to 33%. The increase was mainly due to euro area holdings of portfolio investment equity issued by residents of the United States, which have risen by 286% since the end of 2015, mainly as a result of positive price revaluations. At the same time, euro area holdings of portfolio investment debt securities have increased by 91% since the end of 2015.

The United States is also the largest source country for euro area cross-border financial investment, accounting for bilateral financial liabilities of €8.41 trillion (56% of euro area GDP) at the end of 2024, a 32% increase since the end of 2015. Over the same period, the share of the United States in euro area external liabilities remained broadly stable at 22%. This development mainly reflected an increase of 97% in portfolio investment equity liabilities vis-à-vis the United States, while direct investment liabilities vis-à-vis the United States declined by 9%.

Table 4

Euro area international investment position vis-à-vis the United States

(at the end of the period; non-working day and non-seasonally adjusted)

Source: ECB.

Notes: “p.p.” refers to percentage points. “Equity” comprises equity and investment fund shares. “Total assets/liabilities” refers to the sum of direct investment, portfolio investment, other investment and financial derivatives. Reserve assets are not included in the total. Around 17% of the Eurosystem’s total reserve assets of €1.3 trillion are held in the form of securities, of which an undisclosed part is invested in securities issued in the United States. Financial derivatives are reported separately in gross terms under assets and liabilities. Discrepancies between totals and their components may arise from rounding.

Data revisions

This statistical release incorporates revisions to the data for the reference periods between the first quarter of 2021 and the third quarter of 2024. The revisions reflect revised national contributions to the euro area aggregates because of the incorporation of newly available information.

Next releases

- Monthly balance of payments: 16 April 2025 (reference data up to February 2025)

- Quarterly balance of payments and international investment position: 3 July 2025 (reference data up to the first quarter of 2025)

For queries, please use the Statistical information request form.

Notes

- Data are neither seasonally nor working day-adjusted. Ratios to GDP (including in the charts) refer to four-quarter sums of non-seasonally and non-working day-adjusted GDP figures.

- Hyperlinks in this press release lead to data that may change with subsequent releases as a result of revisions.

Distribution channels: Banking, Finance & Investment Industry

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

Submit your press release