Public vs. private R&D: impacts on productivity

10 January 2025

By Arnaud Dyèvre

This is the third post in our series featuring work submitted to the ECB’s 2024 Young Economist Prize. Arnaud Dyèvre was selected as one of the finalists with the research highlighted in this post. Applications for the 2025 Prize will be open from 13 January to 12 February 2025. For more details, go to the dedicated webpage.

Investments in R&D typically foster productivity growth. But the funding source matters. The ECB Blog shows that publicly funded R&D complements private investments and has greater effects on productivity growth because of its larger spillovers.

Arguably, the track record of government-funded innovation is mixed. On the one hand, governments have funded some technological endeavours that later turned out to be unsuccessful and costly. On the other hand, the history of technology is also filled with crucial innovations developed with public funding: lithium-iron batteries, high-speed trains and the GPS are all either direct results or byproducts of governments providing funding for research and development (R&D). Knowing what sets government funding apart and how it interacts with private R&D is key to our understanding of what drives economic growth.

Comparing private and public R&D funding in the United States between 1950 and 2020, I show in this Blog post that, historically, public R&D tends to produce patents that are more impactful and rely more on science. Furthermore, government-funded R&D has significant spillover effects on the wider economy and a larger impact on productivity. This US experience can be informative for growth and innovation in the euro area, where the need for growth-enhancing policies is more salient than ever after a decade of disappointing productivity growth.

The shift from public to private R&D

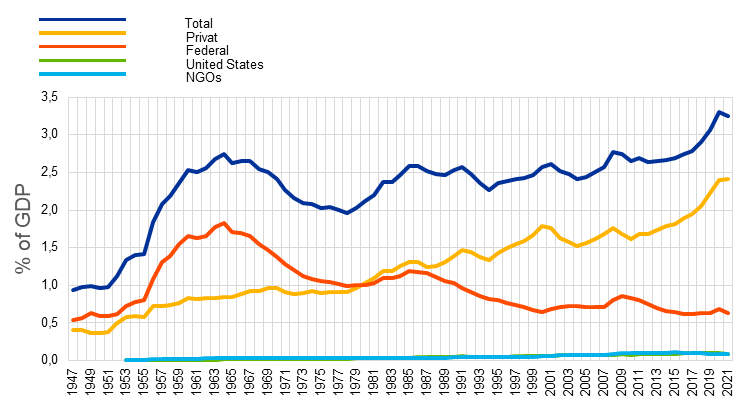

Overall funding for R&D has increased in the United States since the 1950s, but there has been a significant change in its composition (Chart 1). Measured as a share of GDP, R&D that is directly funded by the government (but which may be carried out by private firms, universities or government labs) peaked in 1964 (blue line) and has since diminished by two-thirds. In contrast, private R&D has tripled over the same period (orange line), surpassing government funding as the largest source in 1980. Meanwhile, funding from NGOs, universities, and individual US states has always been marginal.

Chart 1

The shift in US R&D funding from public to private

Source: Paper, based on data from the National Science Foundation.

Key differences between public and private R&D

The implications of this decline in publicly funded R&D become clear when looking at US patent data over the past 70 years, distinguishing between patents funded by public money and those funded by private money.[1] Publicly funded patents differ significantly from those developed with private funding, irrespective of who performs the R&D: firms, universities or government labs.

First, patents funded by public money are much more likely to be grounded in scientific research. They cite scientific papers nearly four times as often as private patents do. This suggests that public patents are more reliant on fundamental knowledge, whereas private firms tend to focus on research with more immediate commercial applications.

Second, publicly funded patents tend to be more impactful than private ones. I measure the impact of a patent by the number of times it is cited by other patents[2] and by its potential to be a breakthrough innovation (that is, a patent that opens an entirely new technology class). Even when adjusting for the financial input and the productivity of the patent’s inventors, I find that publicly funded patents are 19% more likely to be breakthrough innovations than private ones.

Third, and most importantly, public R&D generates greater “spillovers”, meaning that its innovations are beneficial to a greater number of firms across the economy. I measure the extent of a patent’s spillovers by counting the number of patent “technology classes” (i.e. technological categories) that cite this patent. Public patents are, on average, referenced by a larger number of technology classes. For instance, the patent most cited across technology classes was filed in 1989 by a company that received NASA funding and developed microactuators, an invention that found applications in medicine, consumer electronics, aerospace, and many other areas.

While this comparison does not capture all aspects of R&D – at the very least because not all innovations are patented – it does focus my study on innovations with commercial applications. As such, this approach is uniquely suited to understanding the impacts of R&D on firm productivity, which I discuss in the next section.

Public R&D spillovers increase firm productivity

The larger spillovers from publicly funded innovations have significant positive effects on the private sector, boosting firm productivity, further patent production, and additional R&D spending. I find a causal link by examining funding shocks, which I define as all changes in US federal government spending on R&D across agencies and time. These shocks offer a natural experiment akin to a randomised control trial, the standard for establishing causality in science.

The NASA funding surge of the 1960s is a telling example of such shocks. In response to the USSR’s launch of Sputnik in 1957, the US government spent an average of USD 25 billion a year on research initiatives in constant 2020 dollars in the subsequent decade. By comparison, NASA’s 1957 R&D budget was a mere USD 500 million. This surge in funding increased NASA’s patent and research output, which in turn spilled over to the private sector. Companies that produced technologies similar to the ones on which NASA was working had access to a larger flow of knowledge from NASA, which prompted them to produce more patents and invest more in R&D as well.

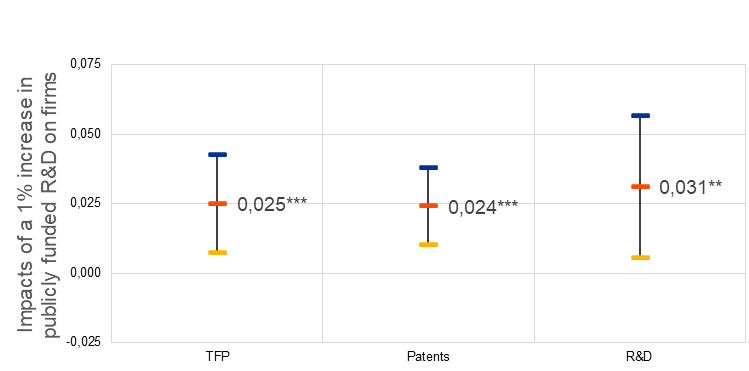

Using these variations in funding as well as firms’ technological proximity to specific federal agencies, I find that a 1% increase in publicly funded patents leads to a 0.025% increase in total factor productivity (TFP), a 0.024% rise in the firms’ own patent output, and a 0.031% increase in their R&D expenditures.[3] These impacts are shown, with confidence intervals, in Chart 2. Confidence intervals show how much statistical noise there is in the data. The wider the intervals, the less confident one can be in the precision of the estimations. Notably, smaller firms, which may lack the resources to conduct fundamental R&D, benefit more from public R&D spillovers than larger firms.

Chart 2

Impacts of public R&D spillovers on firm productivity and innovation

Source: Paper.

Implications for overall productivity

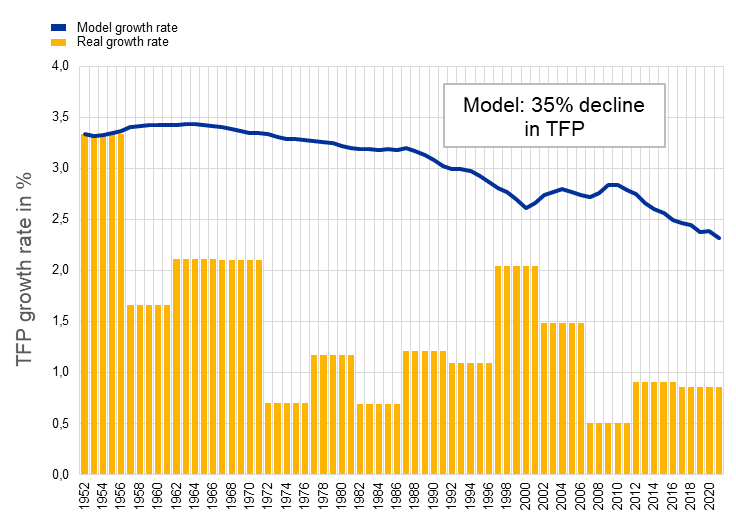

Given the differences between public and private R&D, and the positive impacts of public R&D on firm productivity, could the decline in public R&D be partly responsible for the slowdown in US productivity growth? To evaluate the aggregate consequences of these differences, I built a macroeconomic model of US productivity since 1950, in which both the government and private firms engage in R&D. A key assumption is that the government is more interested in generating breakthrough innovations that may or may not be useful for firms, while firms focus their R&D efforts on more targeted innovation that have a clear potential to improve their own productivity and products. As a result, the government specialises in fundamental R&D while firms specialise in applied R&D. The model is then calibrated with the decline in public R&D we saw in Chart 1, as well as the impact estimates from Chart 2.

The results suggest that around one-third of the decline in productivity growth since 1960 can be attributed to the reduced role of public R&D. Chart 3 shows the declining productivity growth in the United States over the last 70 years (in orange) and the TFP growth predicted by the model (in blue).

Chart 3

US productivity growth; model versus data

Source: Paper.

This does not imply that public R&D is inherently better than private R&D. Instead, they serve complementary roles. Public R&D lays the groundwork through fundamental research, which entrepreneurs then build upon to create marketable products and services. A balanced mix of both types of R&D is essential for driving productivity, but it appears that the United States is currently overly reliant on private R&D.

Which lessons can the euro area and the broader European Union draw from this evidence? In the absence of directly comparable, long-term data in the EU, making EU-specific recommendations is a speculative exercise. One can note, however, that a key issue faced by European innovators is not the lack of public funding of innovation, but rather the lack of venture capital allowing innovators to translate ideas into profitable businesses. This is a core tenet of the recent report by Mario Draghi on the future of European competitiveness, and the strong complementarities between public and private R&D highlighted by this research echo this point.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe for future posts.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

Distribution channels: Banking, Finance & Investment Industry

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

Submit your press release